Now that Value-Based Care (VBC) is the lay of the land, payers, providers and pharma are having to reckon with its shift towards preventive health and behavioral interventions. Digital therapeutics offers one answer for all involved.

Growing Movement

Cognitive behavioral therapy (CBT), long considered the gold standard for anxiety and depression treatment, is now delivered through FDA-cleared apps. Virtual reality is being used for chronic pain management and stroke rehabilitation. Digital and video-based yoga and meditation programs are being studied as adjunct therapies for everything from PTSD to cardiovascular recovery. Digital music-based interventions are tackling some of our most intractable challenges, including dementia and autism spectrum disorders.

Payers Taking Note

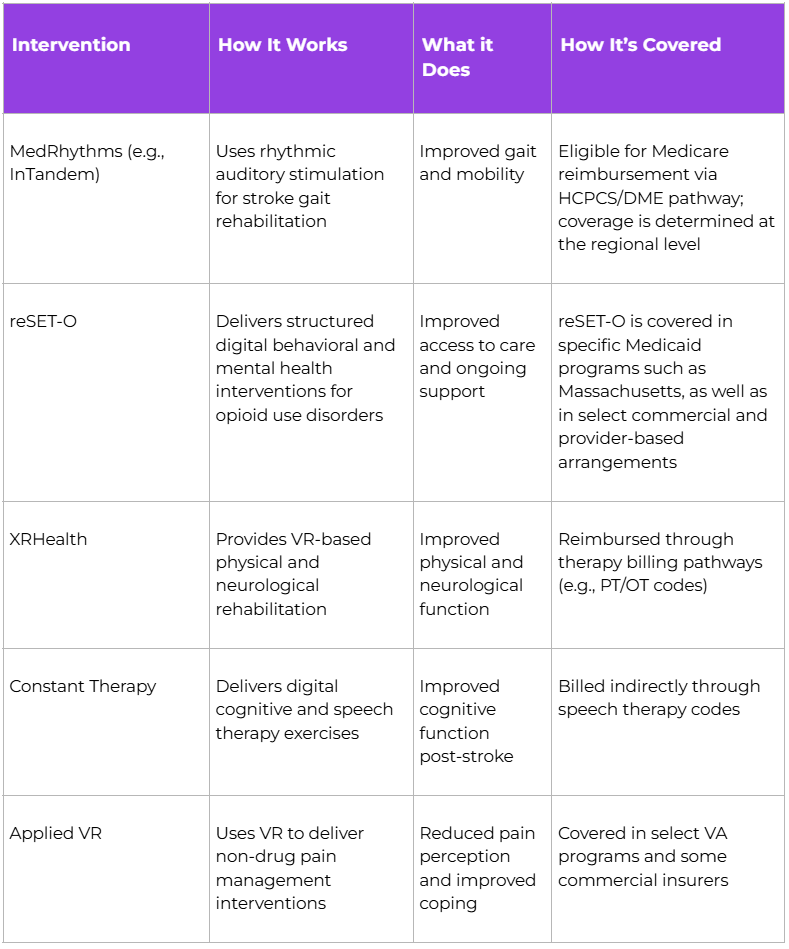

What unites these approaches is a shift that takes digital health from wellness to clinical interventions. The evidence base varies by modality. CBT has decades of robust trials behind it, while music and movement interventions are still building theirs. That said, coverage and reimbursement pathways are gaining ground. For example:

This trend doesn’t constitute a wholesale overhaul of pharmacotherapy. Most of these tools are companions to traditional interventions and medication, not substitutes.

The Value Case

One of the challenges with digital health interventions is perceived misalignments between healthcare players: patients, payers, providers and pharma. Each wonders, who will pay for this innovation and who will reap the rewards? Yet when we examine some of the most successful digital health implementations, there are benefits for every sector of the ecosystem.

For patients and families, it is simple: fewer medications to take and track, as well as better quality of life. In addition, more than four in ten adults over 65 now take five or more prescription medications daily, a figure that has nearly doubled in the past two decades. This has resulted in higher risk of adverse events, increased hospitalizations, and intensifying caregiving burdens (as if they were not already high enough). This is a cycle that VBC is supposed to correct. Conditions like dementia, where pharmacologic options are limited, interventions that improve engagement and reduce isolation offer something medication cannot.

For pharma companies, the opportunity is counterintuitive but real. Digital companion apps do not compete with drugs—they make them work better. They improve adherence, reduce the impact of polypharmacy, and extend the useful life of existing therapies. At a time when VBC is putting a premium on reducing medications, digital health solutions provide new revenue streams, both as companion apps and as standalone solutions. Another upside for pharma is that the regulatory pathways for digital health can be much swifter than those for traditional pharma, making time to market quicker and less cost intensive.

For providers, this is about outcomes and efficiency. These tools extend care beyond the visit and make treatment more engaging. In one pilot of SingFit, patients with dementia receiving music-supported speech therapy attended 2.6 times more sessions than those without the singing-based intervention, because outcomes improved enough to justify continued care. A SingFit pilot study in skilled nursing facilities also showed patients who attended group singing sessions experienced fewer falls, hospitalizations and behavioral health exacerbations than their counterparts. Fewer crises. Fewer interventions. Less strain on staff.

For payers, the shift is structural. Coverage is emerging across supplemental benefits, therapy codes, and other pathways. In models like Institutional Special Needs Plan (I-SNP), tools that improve outcomes while lowering total cost are already being integrated into care.

What Comes Next

As digital health and VBC mature, the goal is not to replace medications, it is to provide the best outcomes with the lowest risk.

The most important signal for these players, however, does not have to do with billing codes, regulatory status or reimbursement pathways, but with consumer demand.

The generation now entering the healthcare system was raised on digital-first experiences. World Economic Forum research shows that 66% of Gen Z use digital tools such as wellness apps and fitness trackers to monitor their health, compared with 40% of older generations.

This means Gen Z and Gen Alpha, raised in a VBC paradigm, will be expecting these tools as part of their healthcare journey. The question is, who will lead the pack in providing these solutions?