Link to full post: GLP-1 Drugs, Digital Health & Obesity Trends in 2026

Overweight and obesity are driving a booming digital health market through telehealth, wearables, and new pharma-to-consumer models.

I've been reporting on this space in my #Trends report since March 2024—two years ago (Navigating Obesity Care in the Digital Age). I’m sensing an inflection point.

New data predicts that 47% of U.S. adults will have obesity by 2035—a burden that doesn't affect all races and ethnicities equally. With novel therapeutics that are remarkably—and I mean remarkably—effective, new business models have sprouted and are now being scrutinized.

Obesity Prevalence and 2035 Projections

In 1990, roughly 1 in 5 American adults had obesity. By 2022, that number had climbed to 42.5%—about 107 million people. A new analysis published in JAMA projects that by 2035, nearly half of U.S. adults (46.9%) will meet the criteria for obesity, with no demographic group spared.

The national average, though, obscures some significant variation. In 2022, non-Hispanic Black females had the highest age-standardized prevalence at 56.9%—nearly 17 percentage points above non-Hispanic White females (41.5%). Hispanic females were at 49.4%. By 2035, non-Hispanic Black females are projected to reach 59.5%.

The steepest rise over the study period was among Hispanic adults. Between 1990 and 2022, obesity prevalence among Hispanic males more than doubled—from 17.4% to 42.6%—with Hispanic females showing nearly identical increases.

Geography matters too. Midwestern and Southern states consistently carry the highest burden. West Virginia, Oklahoma, and Mississippi rank among the worst. States like Colorado and the District of Columbia sit at the lower end.

The drivers behind these disparities are well-documented: structural racism, food insecurity, differential access to safe spaces for physical activity, and socioeconomic deprivation.

For us as clinicians, the 2035 projections map directly onto the chronic disease burden we'll be managing—more diabetes, more cardiovascular disease, more musculoskeletal disease, more Alzheimer's, and higher costs across the board.

Modern Medicine for Obesity

If you've been reading the Huddle for a while, you know I've covered GLP-1s from nearly every angle—their mechanism, their economics, their access barriers, and their adherence problems.

What Are GLP-1s?

GLP-1 receptor agonists (GLP-1 RAs) mimic glucagon-like peptide-1, a hormone released from the gut after eating. It suppress appetite, slows gastric emptying, boosts insulin secretion, and reduces glucagon. This results in less hunger, less food intake, and meaningful weight loss.

The two drugs dominating the conversation right now are:

Semaglutide (Ozempic for T2DM, Wegovy for obesity): a pure GLP-1 agonist. In the STEP-1 trial, it led to ~15% mean weight loss at 68 weeks.

Tirzepatide (Mounjaro for T2DM, Zepbound for obesity): a dual GLP-1/GIP agonist. In SURMOUNT-1, it achieved ~20% mean weight loss.

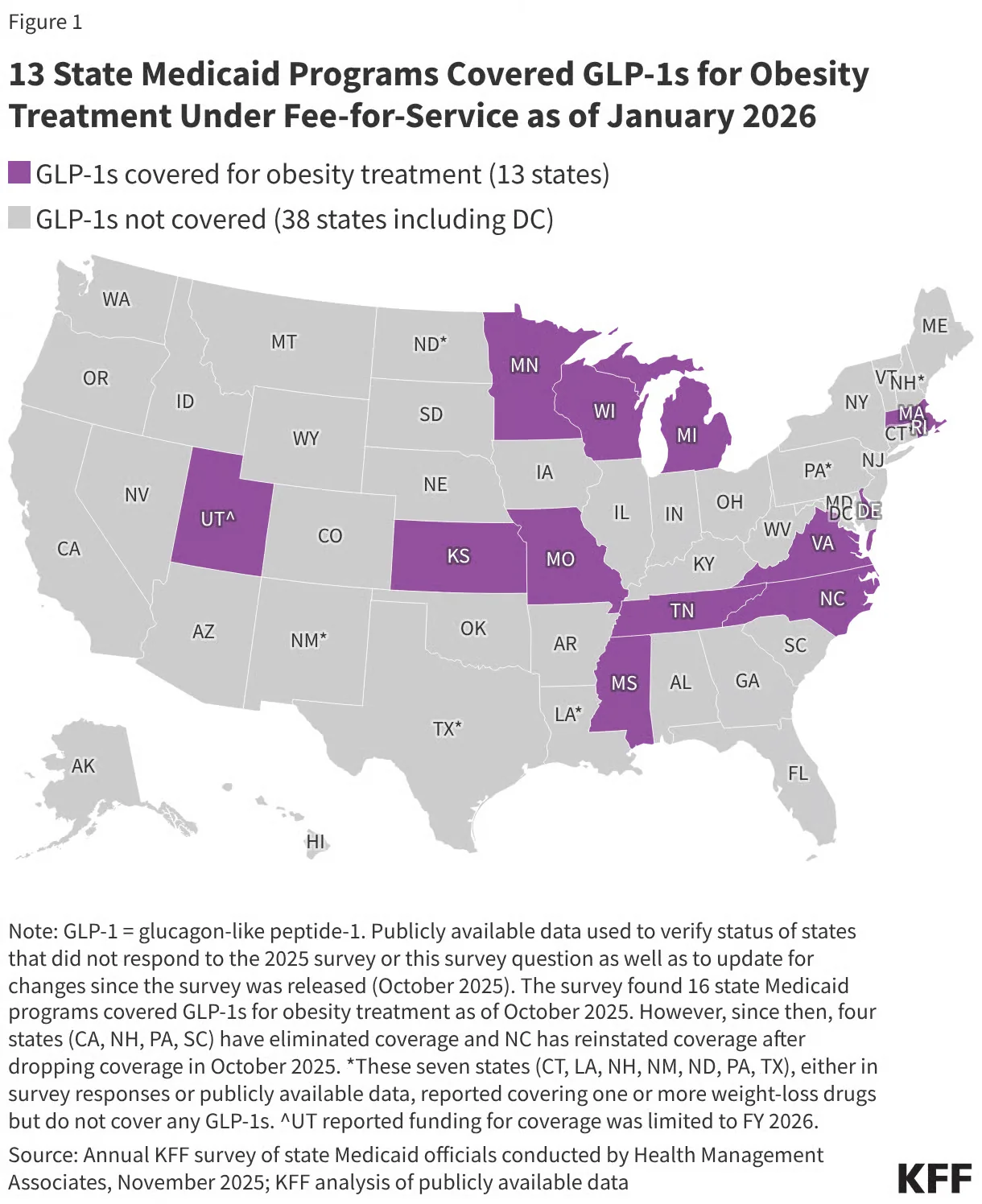

Coverage Issues: Medicare

For years, Medicare has been prohibited from covering weight loss drugs because of the Medicare Prescription Drug, Improvement, and Modernization Act of 2003, which explicitly bars coverage of drugs for weight loss.

The landscape shifted in November 2025. The Trump administration announced negotiated price agreements with Novo Nordisk and Eli Lilly under a new platform called TrumpRx. Ozempic, Wegovy, Mounjaro, and Zepbound will be priced at $245 per month—less than half of prior prices. A bridge payment demonstration kicks off in July 2026, with beneficiaries paying just $50/month in copay.

Medicare's statutory prohibition on covering weight loss drugs hasn't changed, though. If the demonstrations end without Congress acting, coverage goes away.

Adherence Issues

Even when patients can access GLP-1s, staying on them is another challenge.

A JAMA Network Open retrospective cohort study of 125,474 adults with overweight or obesity:

Patients with T2DM:

46.5% discontinued by year one

64.1% discontinued by year two

Patients without T2DM:

64.8% discontinued by year one

84.4% discontinued by year two

Nearly 85% of patients without diabetes stopped taking GLP-1s within two years. The factors driving discontinuation: GI side effects, age ≥65, lower income, and lack of meaningful weight loss early in treatment.

And here's what that means clinically: GLP-1s require long-term use to sustain their benefits. This is no different than blood pressure medication—you need to stay on it for it to work.

The reasons people stop are worth naming plainly:

Cost and coverage gaps: the most common driver.

GI side effects: nausea, vomiting, and diarrhea are common early on.

Goal confusion: some patients stop once they've hit a weight loss target

Access disruptions: drug shortages, prior auth delays, and pharmacy logistics all contribute.

How Digital Health is Impacting Weight Management

The obesity epidemic created a massive market opportunity, and digital health companies moved fast to capture it.

These companies combine GLP-1 access with care coordination, often taking on some degree of outcome accountability.

But access and affordability came with a workaround that's now under serious regulatory fire: compounding pharmacies.

The FDA started running out of patience quickly. In February 2026, Commissioner Marty Makary announced the agency's intent to crack down on non-FDA-approved GLP-1 compounding.

The regulatory crackdown on compounding may improve access for some, but it doesn't address the broader issue: keeping patients on these medications long-term requires infrastructure that most telehealth models weren’t built to provide.

A New Strategy: Pharma's D2C Pivot

The most structurally significant shift may be coming from pharma itself.

Eli Lilly launched LillyDirect to sell Zepbound directly to patients at a self-pay price—cutting out the PBM layer entirely–launching a new employer-connect platform. Novo Nordisk followed with its own D2C pricing through NovoCare, offering Wegovy at $349 cash-pay.

PBMs extract enormous rebates, prior authorization adds friction, and adherence suffers. Going direct lets manufacturers own the relationship with the patient.

The concern is what happens when manufacturers control the prescribing pathway directly.

Dashevsky’s Dissection

Patients benefit greatly from GLP-1 drugs, but adherence remains a challenge. That's why comprehensive care matters—nutrition, coaching, training, and even bariatric surgery when needed.

Some may just want the injectable and nothing more.

As physicians, we're witnessing a historic moment. We have a medication that treats not just obesity, but also diabetes, cardiovascular disease, osteoarthritis, chronic kidney disease, and obstructive sleep apnea.

As for the system—will we see a public health benefit from these GLP-1s? For a public health intervention to be scalable, it needs to be cheap. GLP-1s are not cheap. While GLP-1s are cost-effective for those with diabetes, for those with obesity, these medications are not cost-effective at current prices.

In summary, GLP-1 medications represent a transformative moment in obesity treatment, with proven efficacy across multiple chronic conditions. However, their impact as a true public health intervention remains limited by cost, adherence challenges, and infrastructure gaps in long-term care delivery. Sustainable outcomes will require comprehensive support systems—not just prescriptions.

Jared Dashevsky, MD, is an internal medicine physician and incoming pulmonary and critical care fellow at Mount Sinai, and the founder of Healthcare Huddle — a newsletter read by over 30,000 physicians and healthcare professionals. He writes at the intersection of clinical medicine, health policy, and health technology, translating complex industry dynamics into sharp, evidence-based commentary for busy clinicians. His work covers AI in practice, drug pricing, insurance dysfunction, and the business forces reshaping how medicine is delivered.